Q3 2025 marked a decisive transition for Europe’s crypto market. The quarter was shaped less by price speculation and more by regulatory execution, institutional positioning, and consolidation – forces that are now redefining how capital moves and how information is consumed across the region.

Three dynamics set the tone for the quarter:

- MiCA moved from framework to reality, triggering consolidation as firms prepared for authorization deadlines and the gradual expiry of national “grandfathering” regimes.

- Market leadership rotated, with Ethereum and infrastructure-linked altcoins outperforming Bitcoin amid renewed interest in DeFi, Layer-2 scaling, and real-world asset tokenization.

- Institutional participation deepened, supported by regulatory clarity, ETF inflows, and a growing preference for compliant, Europe-ready platforms.

At the same time, operational requirements under the Digital Operational Resilience Act (DORA) continued to raise the bar for crypto firms, reinforcing a shift toward institutional-grade standards and further thinning the long tail of providers.

These market shifts unfolded alongside a quieter but equally consequential change: how audiences discover crypto information. As search visibility softened and AI-mediated discovery began to reshape referral dynamics, Europe’s crypto media ecosystem entered Q3 facing a new form of pressure – not just to grow, but to remain discoverable.

The result was not uniform decline or recovery, but structural divergence. Traffic, engagement, and visibility began to separate along lines of loyalty, format discipline, and discovery efficiency, with markedly different outcomes across regions and publisher tiers.

What follows examines how these forces played out across Europe’s crypto-native and mainstream media – and why Q3 may prove less a downturn than a reordering of attention.

Methodology: what was measured and why

Outset PR analyzed Similarweb traffic data for 293 news outlets across Eastern and Western Europe, covering both crypto-native publishers and mainstream/non-crypto media with sustained crypto coverage.

The study focuses on Q3 2025 (July-September) to assess how Europe’s crypto mediascape is adjusting to post-search volatility, early GenAI-driven discovery, and increasing tier-based concentration following the sharp contractions observed in Q2.

Media universe

Crypto-native outlets: 200

- Eastern Europe: 109

- Western Europe: 91

Mainstream/non-crypto outlets: 93

- Eastern Europe: 43

- Western Europe: 50

Data interpretation

External traffic estimates may differ from publishers’ internal analytics (e.g., GA4, Adobe, Chartbeat) due to modeled vs. first-party tagging, bot filtering, cookie consent, session rules, subdomain handling, private-share classification, and web-only coverage.

To preserve comparability, the methodology is applied consistently across all outlets and focuses on directional trends. Material anomalies are addressed qualitatively rather than retrofitted to individual dashboards.

Performance benchmarking

Publisher performance is evaluated using Composite Score (CS), which integrates absolute traffic gains, relative growth, and engagement quality into a single standardized metric. The weighting structure remains consistent with prior reports to ensure cross-region and cross-quarter comparability, while allowing room for future refinement as discovery dynamics evolve.

Outlets with under 10K average monthly traffic at the period’s starting point are excluded from composite rankings.

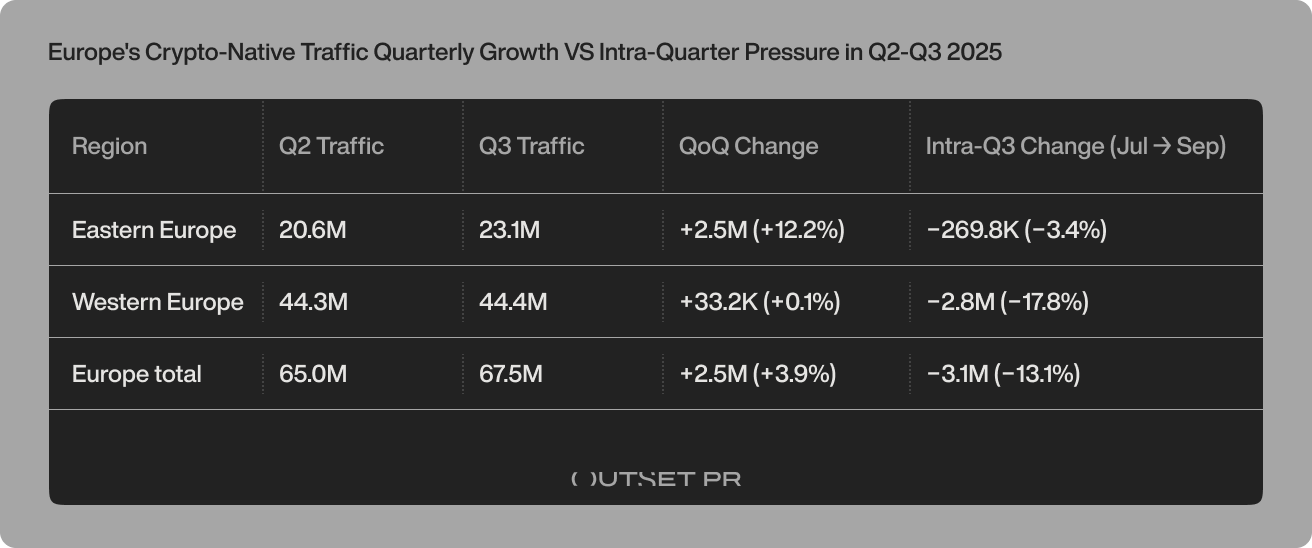

Europe’s crypto-native traffic grew quarter-over-quarter – but intra-quarter pressure persists

Europe’s crypto-native media entered Q3 2025 with a higher baseline than in Q2, resulting in net quarter-over-quarter (QoQ) growth at the aggregate level. At the same time, traffic continued to decline steadily within the quarter, underscoring ongoing discovery pressure and uneven outlet-level performance.

Across Eastern and Western Europe combined, crypto-native publishers recorded 67.51M visits in Q3, up from 64.96M in Q2 – a net increase of 2.55M visits (+3.93% QoQ).

However, this quarterly gain masked a steady decline inside the quarter itself. Traffic fell from 23.84M visits in July to 20.73M in September, representing an intra-quarter loss of 3.11M visits (-13.07%).

- July: 23.84M visits

- August: 22.94M visits

- September: 20.73M visits

At the outlet level, performance remained uneven: 39% of publishers recorded growth, while 61% declined or stagnated, underscoring continued fragmentation between stronger incumbents and a pressured long tail.

Regional momentum diverges beneath the aggregate trend

Q3 did not play out as a uniform recovery or contraction across Europe. Instead, regional momentum diverged, with Eastern and Western Europe contributing differently to quarterly gains and intra-quarter losses.

1. Eastern Europe generated 23.13M visits in Q3, up from 20.61M in Q2, delivering a 2.52M visit increase (+12.23% QoQ).

This marked a clear inflection following the sharp 18% decline recorded in Q2. Within Q3, Eastern Europe experienced only a modest intra-quarter decline, with traffic easing from 7.86M visits in July to 7.59M in September, a loss of 269.8K visits (-3.44%). This indicates aggregate stabilization rather than full recovery, with the region ending the quarter materially stronger than its Q2 baseline despite mild month-to-month pressure.

2. Western Europe recorded 44.38M visits in Q3, compared with 44.35M in Q2, resulting in a near-flat 32.7K visit change (+0.07% QoQ).

Despite maintaining a substantially higher absolute traffic base than Eastern Europe, Western Europe did not contribute meaningfully to Europe’s QoQ growth. Within the quarter, however, the subregion absorbed the majority of Europe’s traffic decline. Visits fell from 15.99M in July to 13.14M in September, a loss of 2.85M visits (-17.80%). This contrast – flat quarterly totals alongside steep intra-quarter erosion – highlights a region where scale masks ongoing volatility.

Mainstream media: scale absorbs the shock

By contrast, mainstream outlets with consistent crypto coverage continued to operate at vastly higher scale:

- Total Q3 traffic: 1.14B visits

- Q3 change: -12.62M (-3.29%)

Only 32.30% of mainstream publications recorded growth, while 67.70% declined or flattened, mirroring crypto-native erosion – but at a far slower proportional pace.

Regionally:

- Eastern Europe mainstream: 850.19M visits (-44.30M vs. Q2)

- Western Europe mainstream: 287.66M visits (-22.23M vs. Q2)

The contrast remains structural: mainstream media absorb large absolute losses without losing dominance, while crypto-native outlets experience sharper percentage swings that more directly affect visibility and strategic relevance.

Takeaway

Q3 2025 confirms that Europe’s crypto-native traffic dynamics are no longer defined by uniform contraction or recovery. Aggregate quarter-over-quarter growth coexisted with continued intra-quarter decline, revealing a market in transition rather than rebound.

Eastern Europe delivered the entirety of Europe’s QoQ growth and showed relative stabilization within the quarter, while Western Europe remained flat on a quarterly basis but absorbed most of the month-to-month decline. At the same time, mainstream media retained scale-driven resilience despite declining volumes, underscoring the widening gap between scale-based insulation and discovery-dependent exposure in Europe’s crypto media ecosystem.

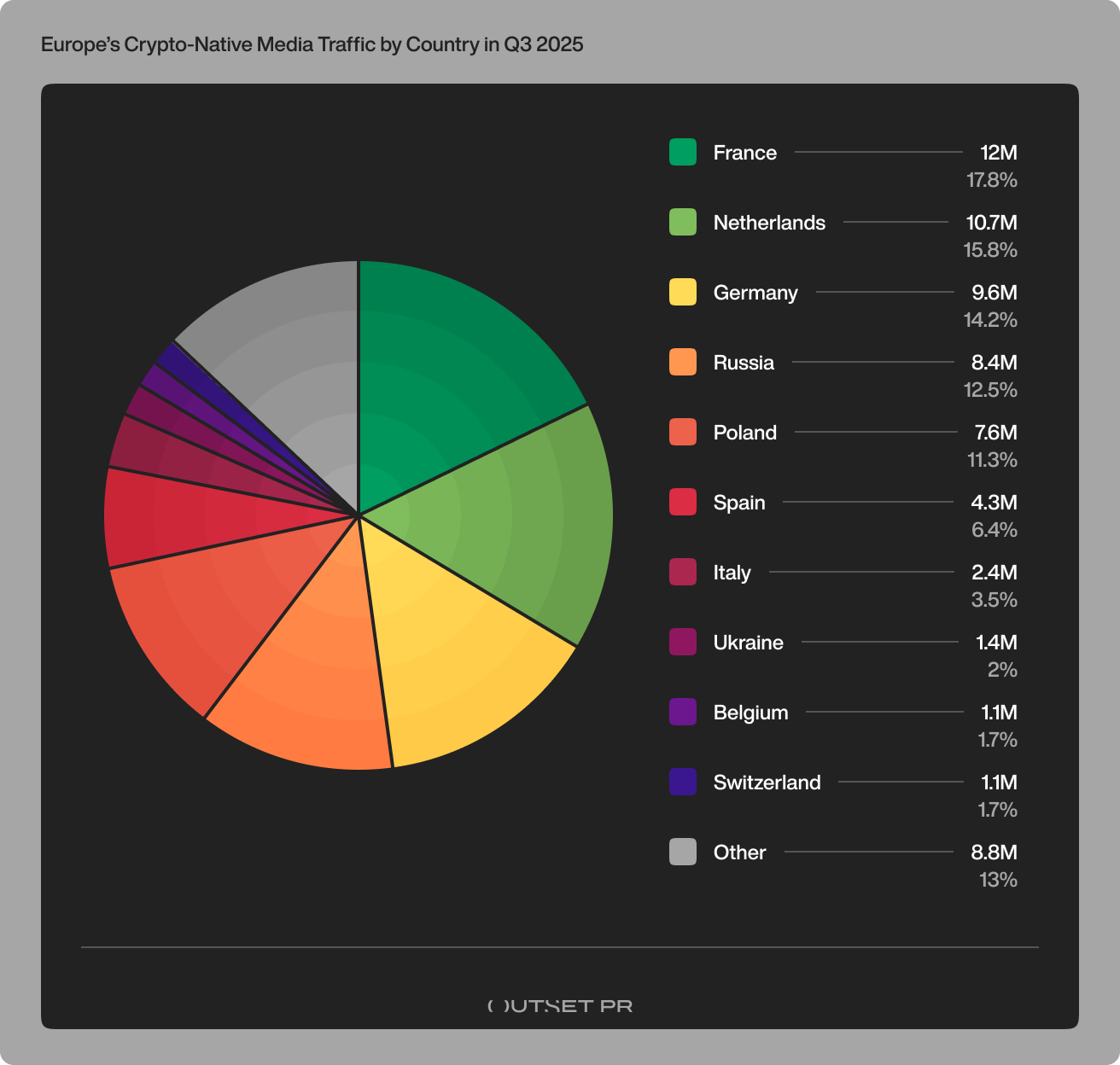

Crypto-native traffic in Europe concentrates across five core markets

- France led Europe with 12.04M visits, accounting for 17.84% of total crypto-native traffic – reflecting strong search-driven visibility across large finance and tech-oriented outlets.

- The Netherlands followed with 10.65M visits (15.78%), driven by a concentration of mid-to-large publishers optimized for organic and aggregator discovery.

- Germany ranked third with 9.61M visits (14.23%), supported by established, compliance-oriented crypto media and strong evergreen coverage.

- Russia remained the largest Eastern European contributor, generating 8.44M visits (12.50%) – underscoring the continued dominance of loyalty-driven, crypto-native readership despite regulatory constraints.

- Poland was close with 7.63M visits (11.30%), largely driven by dominant national outlets and a highly concentrated tier-1 media structure.

Together, these five countries accounted for 71.65% of all crypto-native traffic in Europe during Q3 2025 – highlighting a strongly top-heavy geographic distribution.

- Spain contributed 4.31M visits (6.39%), positioning it as a secondary Western European growth market.

- Italy recorded 2.37M visits (3.51%), reflecting steady but structurally fragmented crypto media consumption.

- Ukraine reached 1.38M visits (2.05%), maintaining visibility in a constrained environment.

- Belgium (1.14M / 1.68%) and Switzerland (1.13M / 1.68%) showed comparable mid-tier footprints, largely tied to pan-European outlets.

- Hungary generated 1.11M visits (1.64%), remaining one of Central Europe’s more visible crypto-native markets.

Smaller but measurable contributions came from Ireland (973.10K / 1.44%), Austria (790.10K / 1.17%), Belarus (752.80K / 1.11%), Slovakia (660.20K / 0.98%), and the Czech Republic (561.50K / 0.83%).

At the far end of the distribution, Bulgaria (208.60K / 0.31%), the UK (159.90K / 0.24%), Romania (94.60K / 0.14%), Latvia (6.95K / 0.01%), Greece (6.25K / 0.01%), and Croatia (5.34K / 0.01%) formed a long tail of marginal but persistent crypto-native readership.

Takeaway

Europe’s crypto-native mediascape in Q3 2025 was geographically concentrated but not singularly dominant. Unlike Asia – where two countries account for the majority of traffic – Europe’s visibility is distributed across five large markets, combining Western Europe’s scale and search discovery with Eastern Europe’s loyalty-driven crypto-native readership.

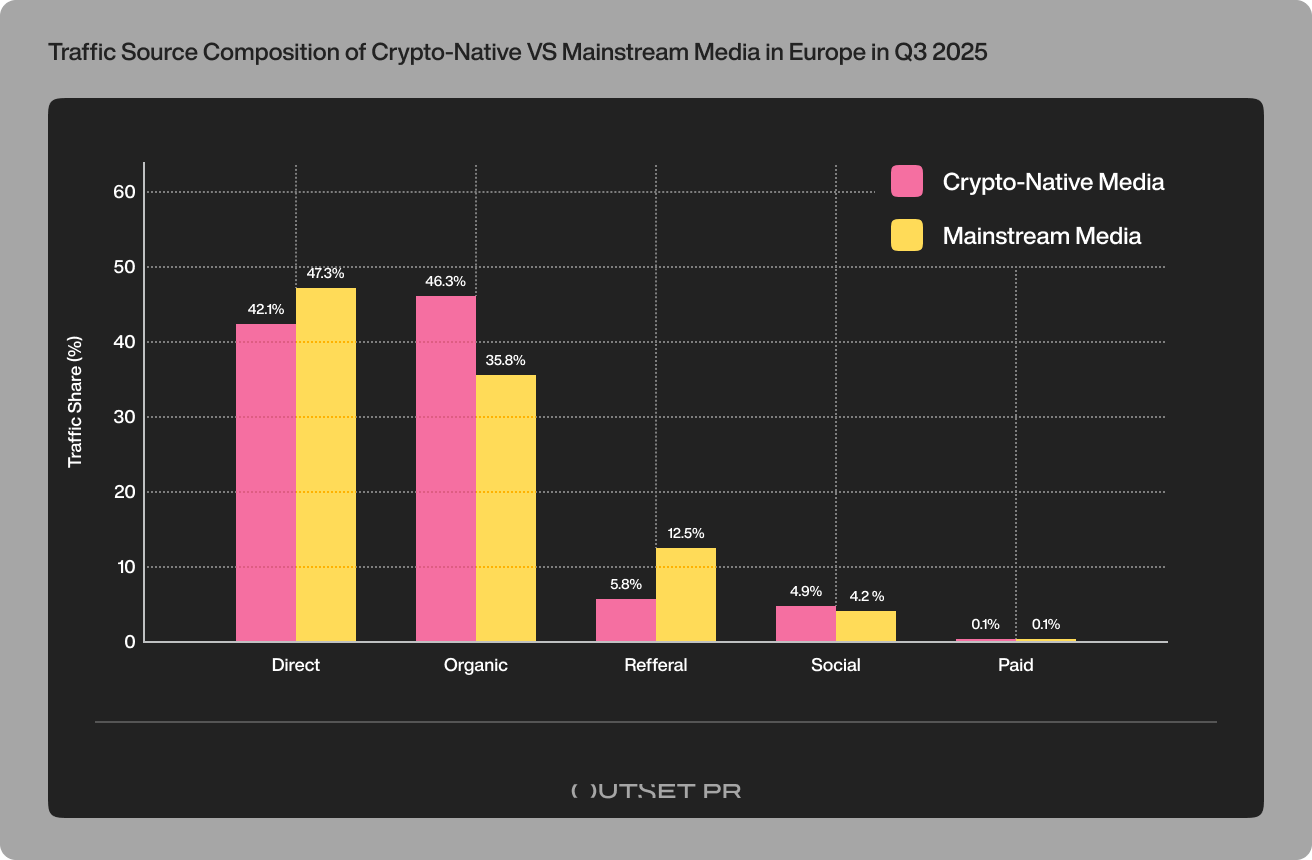

Discovery channels explain why crypto-native traffic is more volatile

In Q3 2025, traffic source composition reveals why crypto-native media experience sharper visibility swings than mainstream outlets.

For crypto-native publishers, discovery remains narrowly concentrated. Organic search delivered 31.27M visits (46.32%), making it the single largest traffic source, while direct traffic accounted for 28.43M visits (42.11%), reflecting a meaningful but limited base of loyal readers.

Together, these two channels dominate crypto-native reach, leaving little structural insulation elsewhere. Referral traffic remained modest at 5.79%, social contributed 4.90%, and paid traffic was negligible at 0.05%, underscoring the sector’s dependence on organic visibility and habitual access.

Mainstream media, by contrast, operate within a far more diversified discovery system. Direct traffic led at 47.28%, supported by organic search at 35.78%, while referrals played a materially larger role, contributing 12.52% of total visits. This broader channel mix allows mainstream outlets to absorb search or platform shocks without experiencing the same proportional volatility.

Takeaway

Crypto-native media in Europe remain discovery-constrained, relying heavily on organic search and direct loyalty channels with limited redundancy in referral or paid sources. This structural constraint amplifies the impact of algorithmic shifts and emerging discovery layers such as GenAI, causing sharper percentage swings in traffic even amid modest absolute declines.

This pattern echoes findings from Asia in Q2 2025, where crypto-native outlets similarly depended on direct and search traffic, and where tier-1 publishers combined loyalty and algorithmic visibility to sustain reach.

In both regions, mid-tier and niche outlets with structured, evergreen content show early signs of adaptation to new discovery logics, while established leaders remain anchored in legacy referral and direct channels.

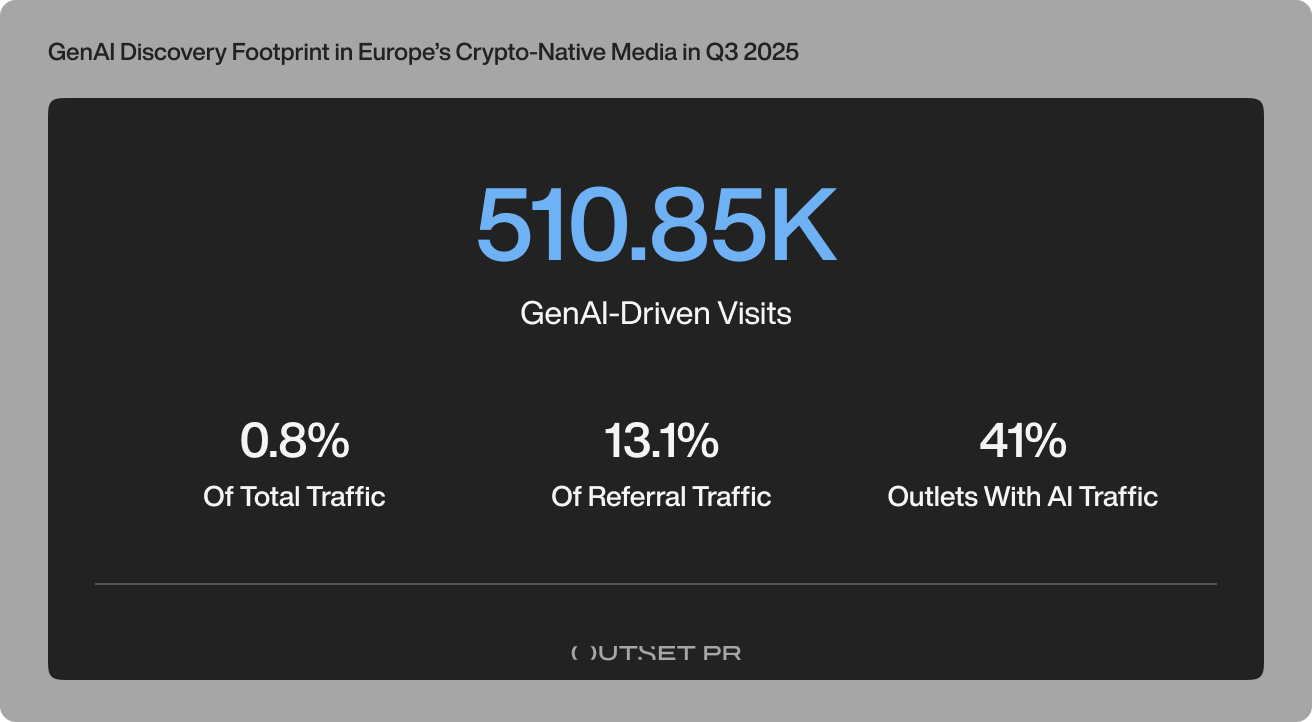

GenAI acts as a visibility filter, not a traffic engine (yet)

GenAI-driven discovery remained a secondary traffic source for Europe’s crypto-native media in Q3 2025, but its structural influence on referral distribution continued to deepen.

Across the quarter, crypto-native outlets recorded an estimated 510.85K GenAI-driven visits, accounting for 0.76% of total crypto-native traffic. While the absolute volume remains limited, GenAI referrals represented 13.07% of total referral traffic, signaling a growing role within the referral layer specifically.

In total, 82 out of 200 crypto-native outlets (41%) recorded measurable traffic from AI-powered interfaces, while 118 outlets (59%) showed no identifiable AI attribution during the quarter.

Where AI visibility concentrates

GenAI exposure is not led by market incumbents, but by the mid and long tail. AI referrals are most prevalent among tier-2 and tier-3 outlets, and the highest reliance appears among publishers focused on:

- evergreen analysis and explainers

- educational or reference-style content

- structured editorial formats with clean metadata and consistent layouts

By contrast, the majority of tier-1 outlets recorded single-digit AI referral shares or none at all, continuing to rely primarily on direct traffic and branded search.

AI-referral intensity

Among the most exposed outlets:

- >60% of referral traffic originated from AI tools in the highest observed cases

- 40-50% among several mid-tier publishers

- 25-35% across a broader group of analytically oriented media

These elevated shares typically coincide with lower absolute traffic volumes, inflating proportional impact without materially shifting total reach.

The most frequently recorded AI referrers were ChatGPT and Perplexity, followed by Gemini, Copilot, and Claude.

Takeaway

In Q3 2025, GenAI discovery in Europe functioned less as a traffic driver and more as a visibility filter:

- It disproportionately surfaces structured, context-rich content

- It rewards semantic clarity and consistency over publishing cadence

- It benefits mid-tier and niche outlets more than established market leaders

While GenAI contributed just 0.76% of total crypto-native traffic, its double-digit share within referrals confirms that AI interfaces are already reshaping discovery mechanics – ahead of any material impact on aggregate volumes.

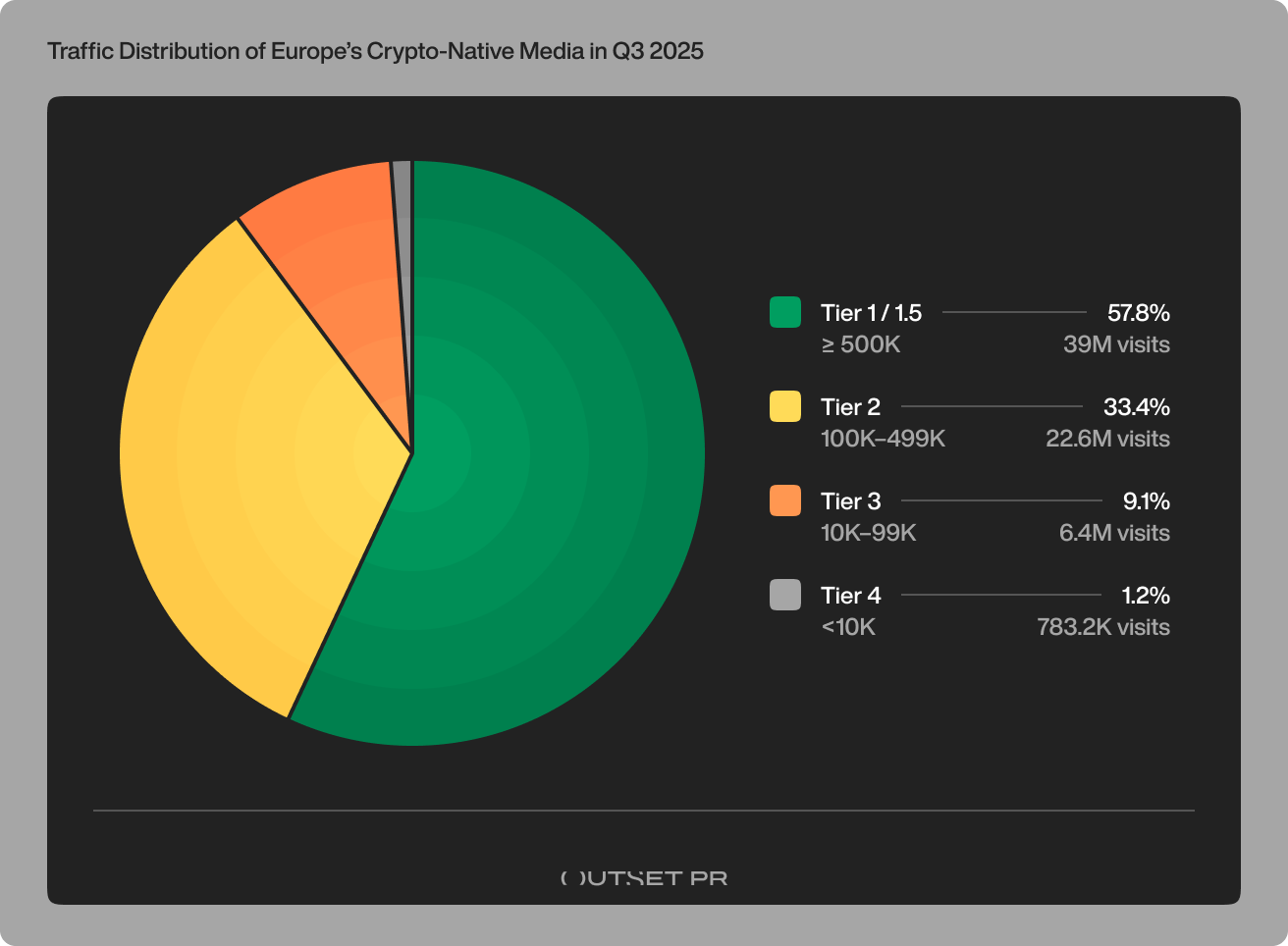

Europe’s crypto-native media stratifies by scale – but discovery logic diverges by tier

Europe’s crypto-native mediascape in Q3 2025 exhibits a clear tier-based stratification, not only in audience scale but also in how visibility is generated and sustained. While top-tier publishers dominate total reach through loyalty and brand gravity, mid-tier outlets increasingly differentiate through format discipline, evergreen content, and early exposure to AI-driven discovery.

Tier 1 / 1.5 (≥ 500K average monthly visits)

These are 12 outlets with 39M Q3 visits, generating 57.80% of crypto-native traffic.

Standout publishers:

- Comparic (Poland)

- CryptoDnes (Bulgaria)

- ForkLog (Russia/CIS)

- BitHub (Poland)

- BTC Echo (Germany)

- Cointelegraph (European editions)

- CryptoNews (pan-European)

- CoinJournal (UK/EU)

They represent Poland, Bulgaria, Russia/CIS, Germany, and pan-EU media hubs, combining loyalty-driven and search-driven dominance.

Tier 2 (100K-499K average monthly visits)

This group includes 32 outlets with 21.90M Q3 visits, contributing 32.40% to the overall crypto-native traffic.

Standout publishers:

- Bits.media (Russia)

- Profinvestment (Russia)

- BitcoinBázis (Hungary)

- Kryptomagazin (Slovakia / Czech Republic)

- CoinTribune (France)

- CryptoNews Poland (Poland)

- Criptovaluta.it (Italy)

The mid tier captures France, Italy, Central Europe, and CIS, and is the primary experimentation layer for AI-driven discovery.

Tier 3 (10K-99K average monthly visits)

The sector is represented by 61 outlets with 6.13M Q3 visits, bringing 9.10% of crypto-native traffic.

Standout publishers:

- Kryptonovinky (CZ / SK)

- HappyCoin (Russia / CIS)

- Crypto.ro (Romania)

- KriptoWorld (Hungary)

- Block-Chain24 (Germany)

- CryptoRussia (Russia)

Tier 4 (<10K average monthly visits)

These are 101 outlets with 0.78M Q3 visits and a 1.16% share in crypto-native traffic.

Standout publishers:

- Cryptonica

- TTRCoin

- Majning-Bitcoin

- 2BMiner

- OKChanger

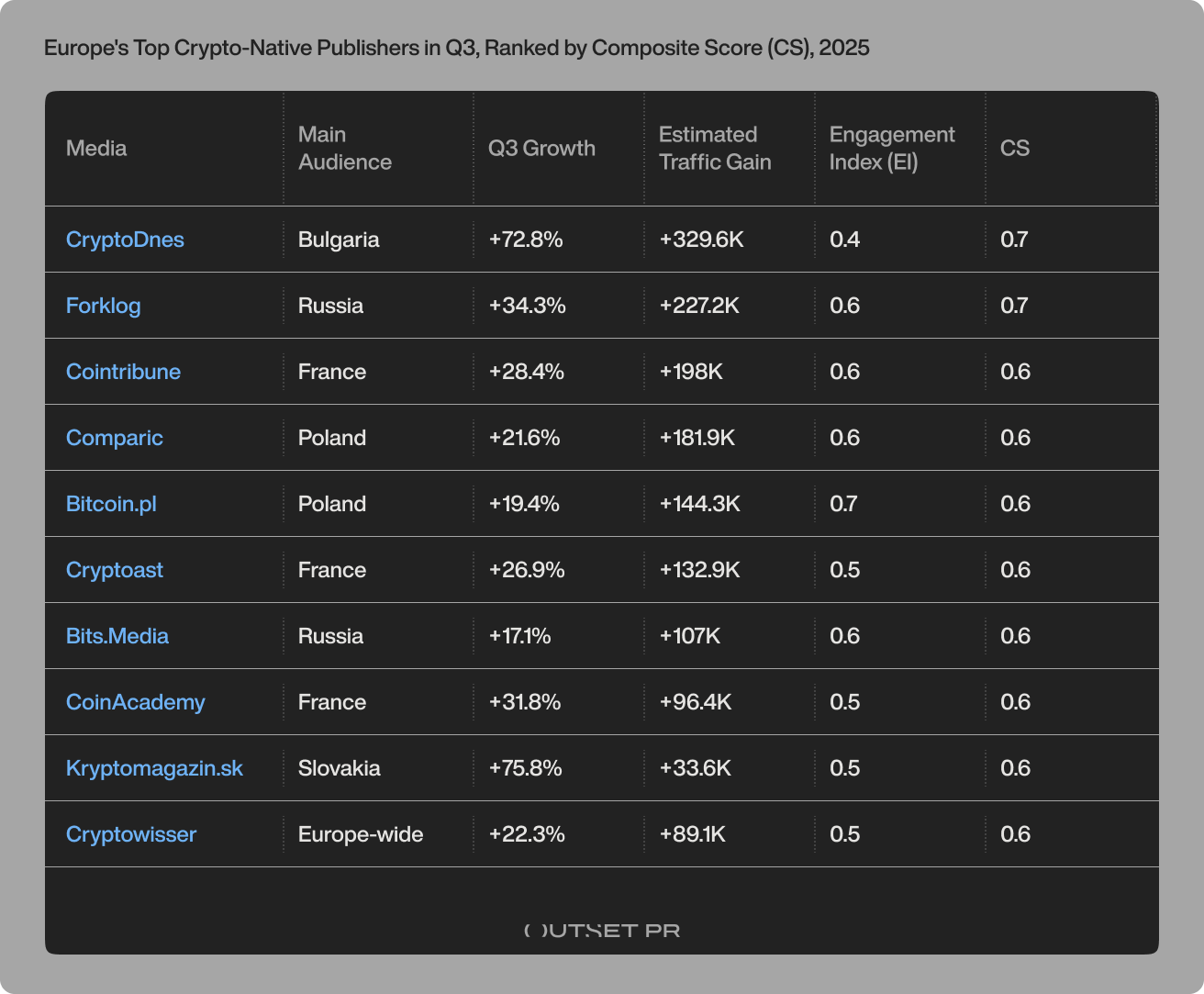

Top-10 crypto-native publishers in Europe by Composite Score (CS)

Despite an overall contraction in Europe’s crypto-native media traffic during Q3 2025, a limited group of publishers achieved meaningful positive momentum, standing out through a combination of scale recovery, structural visibility, and engagement resilience.

Publishers in this section are ranked using Composite Score (CS) – a standardized complex metric developed by Outset PR to assess crypto-native media performance beyond raw traffic size.

CS combines absolute traffic gains (55%), relative growth momentum (25%), and engagement quality (20%) into a single score, balancing scale, growth dynamics, and audience depth.

Note: In earlier reports, this metric was referred to as Refined Composite Score (RCS). The naming has since been consolidated to reflect its role as a stable, reusable benchmark. While the structure of CS remains consistent for cross-report comparability, the methodology may be further refined over time as discovery channels, audience behavior, and data availability evolve.

Eastern Europe: scale-driven recoveries

Several Eastern European publishers ranked among the strongest CS gainers due to absolute traffic recovery amplified by loyal, repeat audiences.

- Forklog rebounded with a net gain of 198.04K visits, supported by 60.02% direct traffic, an average visit duration of 3:17, and 2.58 pages per visit. Growth was driven less by acquisition efficiency than by habitual readership returning after earlier declines.

- CryptoDnes added 146.31K visits, benefiting from strong organic visibility (59.85%) and stable engagement metrics (0:57 average visit duration, 2.05 pages per visit). While engagement depth remains moderate, scale recovery positioned the outlet as a top-tier gainer under CS weighting.

Note: CryptoDnes benefited from international audience expansion. The launch of a Japanese-language edition in early 2025 led to a notable influx of Japanese traffic, materially contributing to the outlet’s strong Q3 growth.

- Bits.media recorded +121.44K visits, combining 51.68% direct traffic with above-average session depth (1:16 average duration, 2.41 pages per visit), reinforcing its role as a trust-based destination within the Russian-speaking crypto ecosystem.

Growth in Eastern Europe is primarily driven by audience loyalty and scale elasticity, where established brands convert modest rebounds into large absolute gains.

Western Europe: momentum and structural efficiency

In Western Europe, CS gainers were shaped less by raw scale and more by search-aligned structure, acquisition efficiency, and engagement consistency.

- Cointribune posted a gain of 214.77K visits, driven by 61.49% organic search and sustained engagement (1:26 average duration, 1.73 pages per visit). Its performance reflects effective alignment with Google and AI-mediated discovery.

- Cryptoast grew by 97.62K visits, combining balanced traffic sources with low bounce rates (39.66%) and consistent session depth, signaling efficient conversion of search visibility into retained readership.

- CoinAcademy added 83.41K visits, supported by 55.54% organic traffic and improving engagement efficiency, positioning it as a structurally optimized mid-to-upper-tier performer.

Western European growth is driven by momentum mechanics – publishers that convert structured discoverability into incremental gains even without dominant direct traffic shares.

Takeaway

CS gainers in Q3 2025 fall into two distinct but equally viable models:

- Scale + trust (Eastern Europe): large audiences magnify recoveries even when engagement depth is average.

- Structure + momentum (Western Europe): optimized formats enable smaller publishers to grow efficiently in a constrained attention environment.

Together, these gainers illustrate that positive growth in Europe’s crypto-native media is no longer broad-based, but conditional – dependent on either entrenched loyalty or structural discoverability.

Go deeper with the full dataset

This report is part of Outset Data Pulse, our ongoing initiative to map how crypto media ecosystems evolve across regions as regulation, discovery, and audience behavior change.

While this edition highlights key trends and top-performing outlets across Europe in Q3 2025, the same analytical frameworks applied here – including tiering logic, traffic source analysis, and the Composite Score (CS) – extend across the full dataset of 293 European media, spanning both crypto-native and mainstream publications.

The dataset includes granular, outlet-level inputs such as visits, growth dynamics, traffic source composition, visit duration, pages per visit, and bounce rate, enabling deeper comparative analysis beyond the snapshots presented in this report.

Using the full Europe Q3 2025 dataset, you can:

- Reconstruct rankings across Europe’s crypto mediascape or isolate specific subsets by country, region (EEU vs. WEU), traffic tier, or publisher type (crypto-native vs. mainstream).

- Track shifts in engagement quality and audience loyalty as Europe’s media ecosystem adjusts to post-search volatility, regulatory execution under MiCA, and rising concentration at the top tiers.

- Compare resilience patterns between crypto-native and mainstream media, identifying where scale, diversification, or structural discoverability dampens the impact of algorithmic and AI-driven discovery changes.

- Test alternative performance scenarios by adjusting outlet cohorts or re-weighting growth, scale, and engagement inputs – enabling tailored analysis for regional planning, media selection, or strategic forecasting.

Beyond headline metrics, this report is designed as a practical decision-making reference for multiple stakeholders operating in Europe’s crypto ecosystem:

- PR and communications teams can use the data to assess where media visibility is structurally resilient versus transient, helping prioritize outlets, regions, and tiers that offer sustained reach rather than short-lived exposure.

- Marketing and business development teams can identify which markets and publisher tiers convert traffic into repeat engagement, informing channel selection, budget allocation, and go-to-market sequencing.

- Investors and analysts can evaluate how media concentration, regulatory execution, and discovery mechanics interact – providing an indirect signal of market maturity, consolidation pressure, and long-term infrastructure viability.

- Publishers, editors, and policymakers can observe how AI-mediated discovery, platform dependency, and regulatory asymmetry are reshaping Europe’s crypto information landscape, highlighting where structural adaptation is already underway and where fragility remains.

At Outset PR, we use this intelligence to inform our own strategies – but we don’t view it as a closed asset. Our aim is to make this data a shared foundation for understanding how crypto media visibility is built, lost, and sustained in a rapidly reordering environment.

Check the full dataset:

As seen in: Altcoin Buzz, Bitzo, Bitcoin Sistemi, Bitcoin Bazis, crypto.news, Crypto Daily, Crypto.ro, Coin Insight, Cointribune, FinanceFeeds, Guia do Investidor, Happy Coin News, MPOST, The Cryptonomist, MarsBit, Smart-Lab, TechBullion, The Blockopedia, Tin Tuc Bitcoin