The second quarter of 2025 marked a significant rebound for the global crypto market. After a sharp 18% drop in Q1, crypto assets delivered a 21.72% return – outperforming equity benchmarks like the S&P 500 and reigniting investor confidence. This momentum was driven by rising institutional interest, growing ETF inflows, and a wave of corporate Bitcoin acquisitions. In the U.S., regulators eased restrictions on banks and crypto firms, rolled back IRS tax enforcement rules affecting individual investors, and advanced the long-debated Market Structure Bill, which aims to establish a comprehensive regulatory framework for digital assets.

Stablecoin adoption also accelerated across small businesses and enterprises, supported by Circle’s landmark IPO and looser U.S. regulatory conditions. Globally, the macro backdrop remained tense: geopolitical shocks, trade disruption, and delayed interest rate cuts created a volatile but opportunity-rich environment. Together, these factors fostered a cautious yet constructive market mood by late Q2, marked by declining speculation and early signs of consolidation.

In Eastern Europe, the media space reflected a more complex interplay of rebound and resistance. Publishers in Poland and Hungary faced mounting pressure to comply with EU regulations such as MiCA, while also contending with visibility fluctuations driven by search algorithm updates. Romanian outlets leaned on consistent publishing formats and aggregator traction to sustain reach, whereas Bulgaria saw overall media traffic growth – much of it originating from outside the country – revealing both the potential and fragility of hybrid content models.

Further east, national constraints played a more dominant role. In Ukraine, the war continued to shape editorial focus, but a June proposal to allow Bitcoin and other digital assets into the National Bank’s reserves signaled long-term strategic intent. In Russia, while mining gained legal ground, crypto media remained bound by strict advertising bans and informal editorial redlines. Belarus remained highly sensitive, with many outlets adapting content formats or relocating hosting infrastructure to stay active.

Across the region, generative AI tools began transforming how users discover content, adding a new layer of complexity to an already evolving media environment. These conditions – global recovery layered with regional disruption – set the stage for an uneven yet revealing quarter for Eastern Europe’s crypto mediascape.

Method and scope: What was measured, and why

This report is based on publicly available traffic estimates from SimilarWeb, aggregated and analyzed by Outset PR’s analytics desk. We reviewed traffic dynamics for 155 media outlets with crypto-related coverage across Eastern Europe during Q2 2025.

The report’s regional scope includes the following countries classified as part of Eastern Europe: Albania, Belarus, Bosnia, Bulgaria, Croatia, the Czech Republic, Estonia, Greece, Hungary, Latvia, Lithuania, Moldova, Poland, Romania, Russia, Serbia, Slovakia, Slovenia, and Ukraine.

Note: While some countries covered in this report – such as Russia, Belarus, and Moldova – are formally or historically associated with the Commonwealth of Independent States (CIS), we include them here as part of Eastern Europe due to their geographic location and editorial alignment with the region’s crypto mediascape.

For clearer analysis of how specialized vs diversified media outlets perform, we categorized media into two core groups:

- Crypto-native outlets (114): Media brands with a primary focus on blockchain, cryptocurrencies, or Web3.

- Non-crypto outlets (43): Finance, general news, and technology media that regularly publish crypto content alongside broader editorial coverage.

Average traffic was calculated from monthly desktop and mobile visits. Quarterly deltas were used to identify growth patterns and structural shifts. Media sites were further segmented by traffic tiers and referral structure to assess decentralization, exposure, and visibility dynamics across the region.

We segmented Eastern Europe’s crypto news outlets across several dimensions:

- Audience geography – inferred from site language, domain extension, and SimilarWeb geolocation data

- Traffic volume tiers – categorized into four groups based on average monthly visits during the quarter

- Traffic source composition – segmented into five categories including Direct Traffic (e.g., bookmarks and typed URLs), Organic (unpaid search engine results), Paid (programmatic ads, sponsored posts, and retargeting), Referral (third-party websites, crypto aggregators, and GenAI platforms such as ChatGPT, Perplexity, and Gemini) and Social (traffic from platforms like Facebook, YouTube, X, and others)

Note: These overlapping layers allowed for a more nuanced view of editorial decentralization, market exposure, and structural differences between crypto-native and non-crypto media operating in the region.

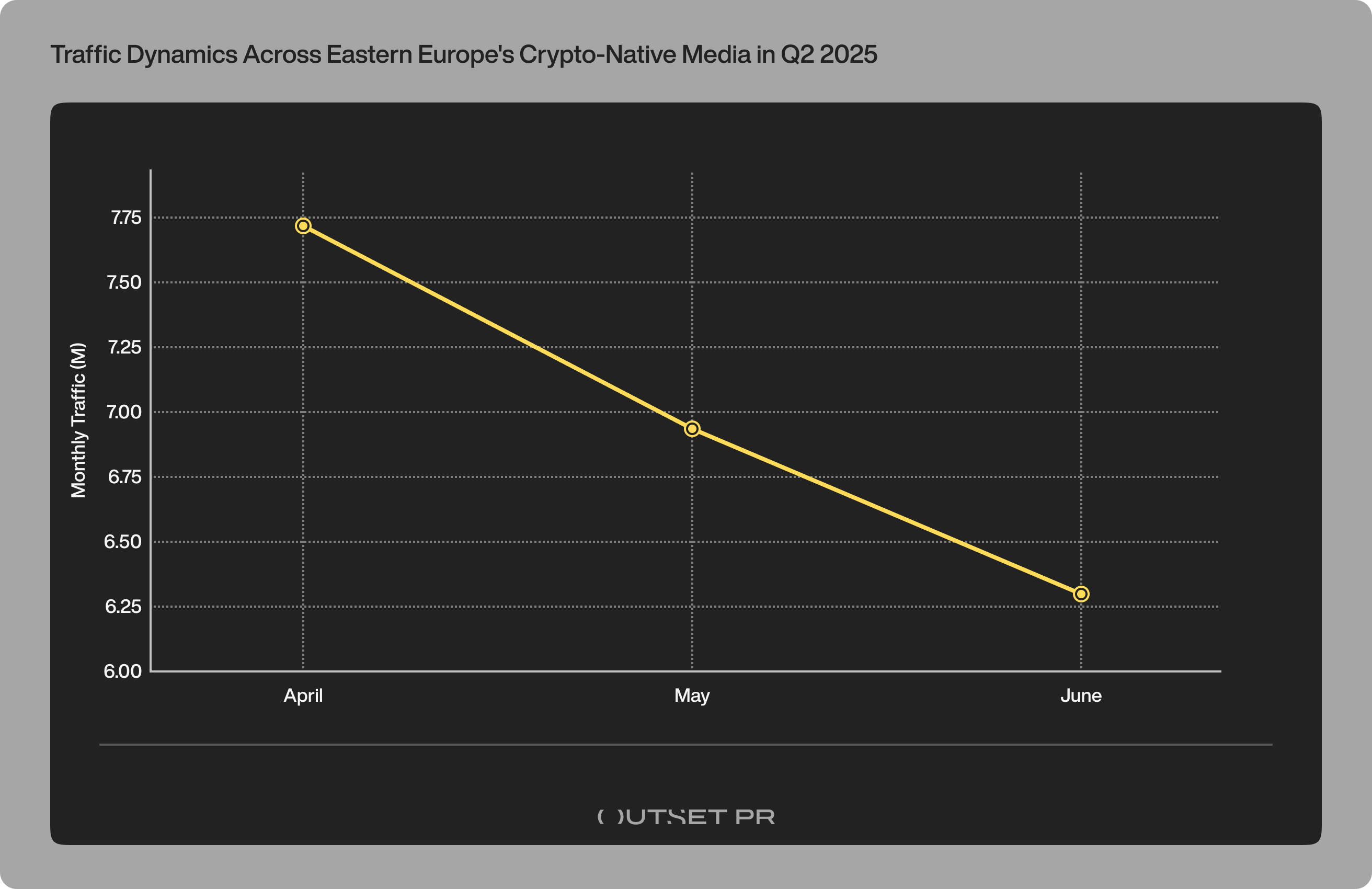

Crypto-native media declined 18% in Q2, but a select few are gaining ground

Crypto-focused publishers faced persistent visibility challenges throughout Q2:

- April 2025: 7.72M visits

- May 2025: 6.88M visits (a decline of 10.77% compared to April)

- June 2025: 6.30M visits (a further drop of 8.43% from May)

This downward trend reflects a cumulative decline of 18.29%, with no meaningful rebound over the quarter. In total, crypto-native outlets recorded 20.89M visits in Q2 2025. Only 36.90% of outlets experienced growth, while 63.10% saw traffic decline.

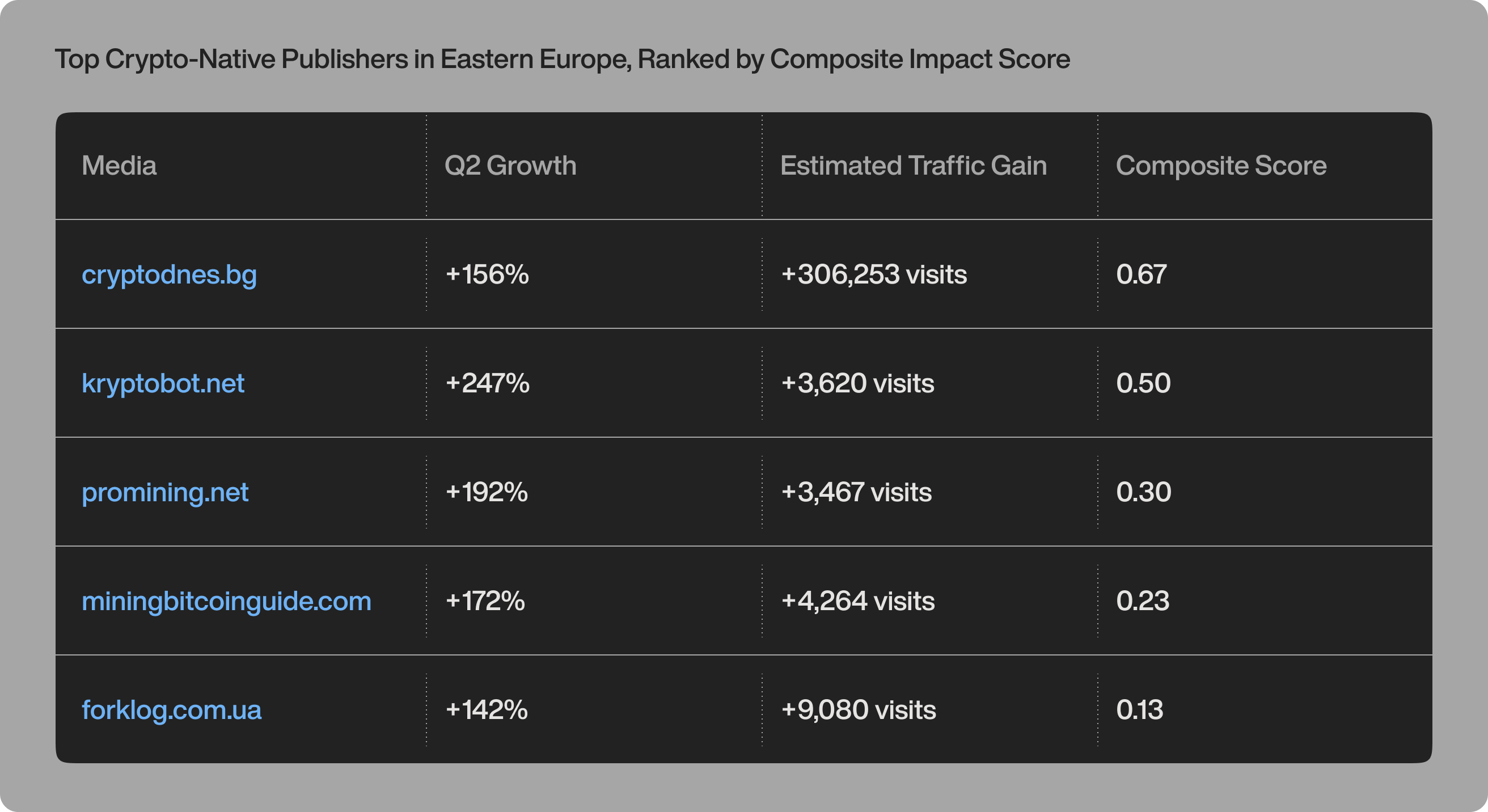

To spotlight the most meaningful growth across Eastern Europe’s crypto-native mediascape, we used a refined methodology based on a composite scoring system that balances two key indicators:

- Relative growth — the percentage increase in traffic from April to June 2025

- Absolute traffic gain — the actual number of new visits acquired during the quarter

Composite Score = (Relative Growth ÷ Max Growth) × 0.3 + (Absolute Gain ÷ Max Gain) × 0.7

We assign 30% weight to relative growth, as it highlights momentum – particularly for outlets gaining visibility within the quarter. However, absolute gain carries 70% weight, since large visit increases reflect more real-world impact and sustained reach, which matters most for strategic media planning.

Note: Relying on percentage growth alone can be misleading, as it favors small outlets with minimal starting traffic. For example, a site jumping from 100 to 400 visits posts +300% growth, but it’s not strategically significant. Using only traffic gain highlights the biggest players, but misses rising outlets gaining momentum that may soon matter more. By combining both metrics into a single composite score, we prioritize sustainable, scalable growth – surfacing outlets that are both gaining reach and accelerating in visibility.

This methodology allows us to highlight breakout publishers that are rising fast and reaching broader audiences – a signal of growing influence worth watching.

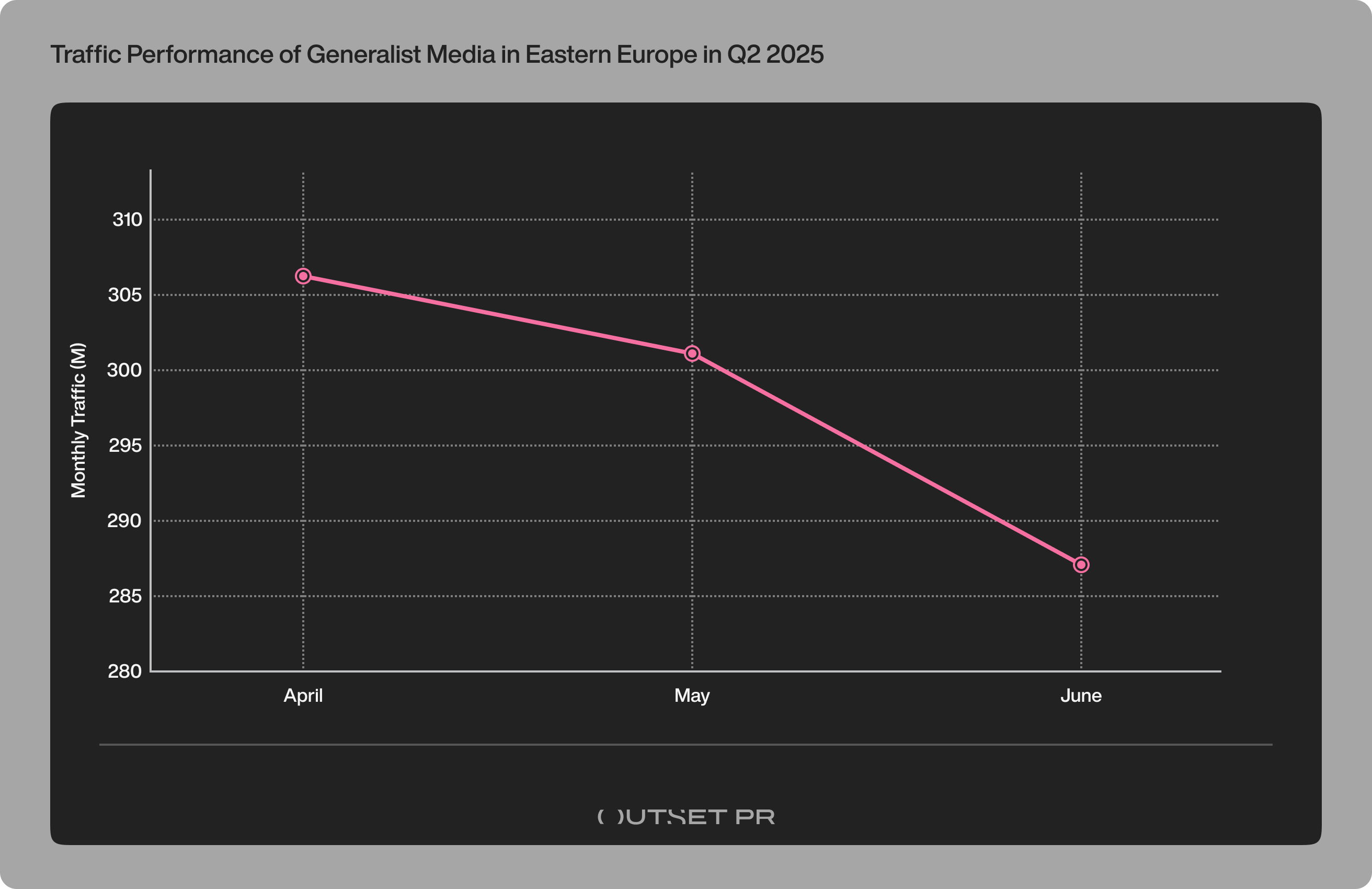

Mainstream media saw milder decline, but traffic losses persisted

Finance, general news, and tech platforms with crypto sections fared better in Q2 2025, though they too experienced gradual month-over-month (MoM) declines. Their broader content portfolios and stronger brand equity helped preserve overall scale – but they were not immune to broader audience fatigue.

- April 2025: 306.21M visits

- May 2025: 301.16M visits (a decline of 1.65% compared to April)

- June 2025: 287.12M (a further drop of 4.66% from May)

In total, generalist media outlets recorded 894.48M visits during Q2 2025.

Similarly to crypto-native outlets, 37.50% of Eastern Europe’s generalist media showed positive momentum, while 62.50% faced traffic losses in Q2 2025 – highlighting a consistent erosion of user activity.

These shifts echo — but do not fully mirror – earlier patterns observed in other regions. In Western Europe, Q1 2025 report revealed a sharp divergence: 81.61% of crypto-native media declined, while generalist outlets remained largely resilient, with 54.35% recording traffic growth despite the challenging discovery environment.

By contrast, Latin America showed a broader downturn: in Q1 2025, 72.73% of crypto-native outlets lost traffic, and generalist media were not immune – with 70.59% of publishers facing erosion amid search algorithm updates and market volatility.

What makes Eastern Europe notable is the consistency across both segments – suggesting that broader editorial scope did not significantly buffer against shifting user behavior or discovery trends in the region.

This overlap between crypto-native and generalist trends also opens the door to identifying exceptions within the generalist space – outlets that bucked the overall pattern and posted meaningful growth.

While our composite score methodology is primarily designed for crypto-native media, it can also be effectively applied to generalist platforms in select cases – particularly those showing exceptional and scalable growth, as well as clear potential for crypto relevance or financial alignment.

One such case is Monitorfx.pl, a Polish generalist finance outlet that demonstrated breakout momentum in Q2 2025. Its traffic rose from just 4,589 visits in March (the only recorded Q1 datapoint) to a total of 54,334 visits in Q2, with MoM growth from 1,092 in April to 38,139 in June.

This represents:

- An absolute gain of +49,745 visits compared to March

- An explosive relative growth of +3,393% between April and June

- A composite score of 0.30, reflecting strong momentum from a low base

While its overall traffic remains modest, the pace and consistency of growth position Monitorfx.pl as a potential rising player in the regional generalist mediascape. Its trajectory illustrates why composite scoring helps surface early signals of momentum, even in outlets still operating at small scale.

Note: We do not apply this method broadly across generalist media. Unless a platform's traffic patterns are clearly tied to crypto-related content, applying composite scoring indiscriminately risks overestimating strategic relevance for crypto PR planning. In all such cases, content focus and audience context remain essential filters.

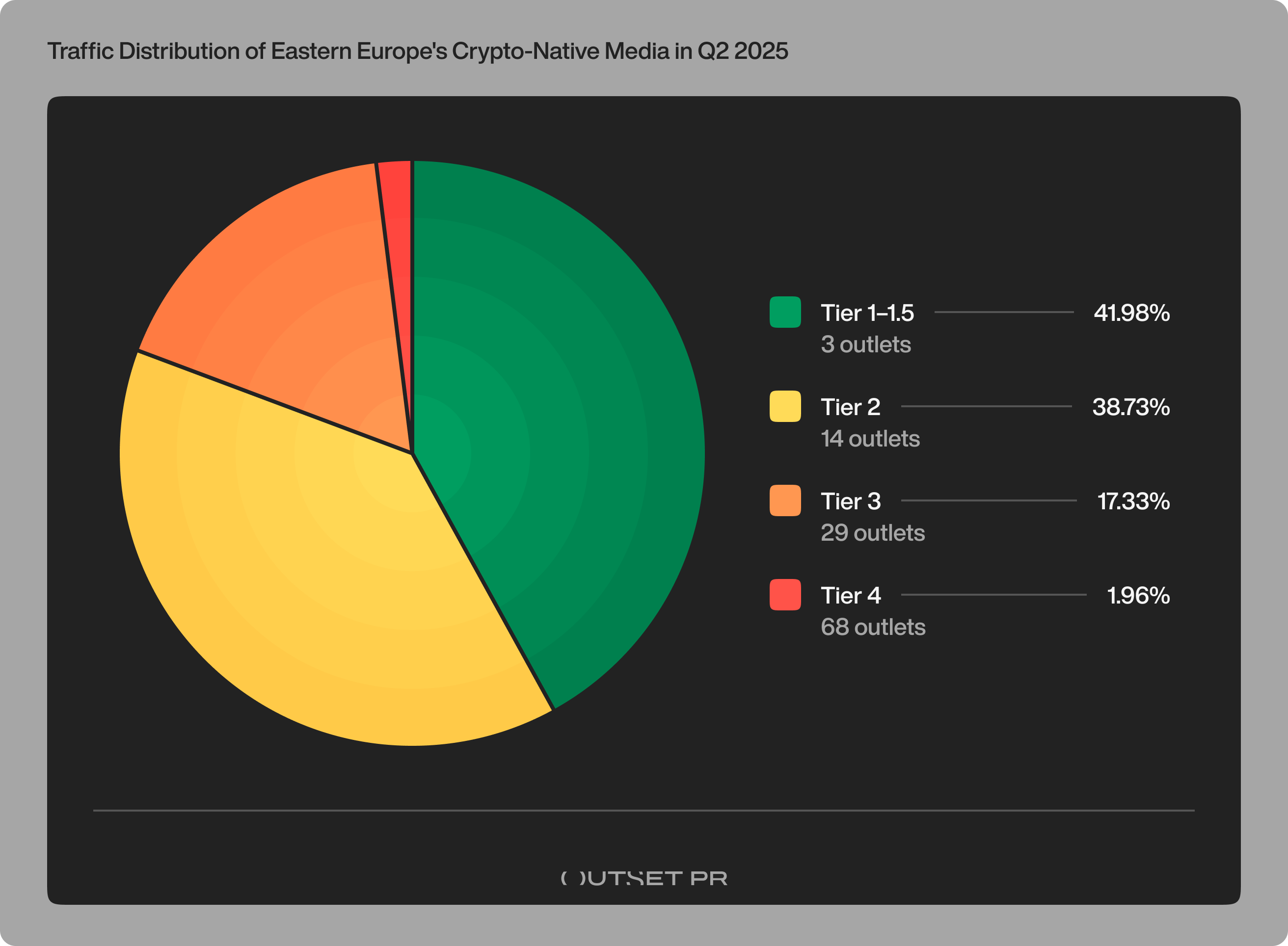

80% Eastern Europe’s сrypto-native traffic comes from just 17 outlets

In Q2 2025, Eastern Europe’s crypto-native mediascape showed a clear pattern of audience consolidation – where just 17 outlets captured 80.71% of the region’s total crypto-native traffic.

We applied Outset PR’s tiering framework, based on average monthly traffic – a method consistently used across our regional media analyses. While tier boundaries are not absolute, they serve as a practical tool for segmenting outlets by scale, reach, and PR impact.

The four tiers used in this report are as follows:

- Tier 1+1.5: 500K+ monthly visits

- Tier 2: 100K-499K monthly visits

- Tier 3: 100-99K monthly visits

- Tier 4: Below 10K monthly visits

When outlets are sorted into these tiers, the Q2 traffic distribution in Eastern Europe reveals the following structure:

Three tier 1-1.5 outlets, each averaging over 500K monthly visits, collectively generated 8.77M visits in Q2, accounting for 41.98% of total crypto-native media traffic in the region:

- comparic.pl

- bithub.pl

- forklog.com

The Polish outlet Comparic.pl stood out as the only crypto-native publication in Eastern Europe to exceed 1M average monthly visits, reaching 1.35M monthly on average and totaling 4.05M over the quarter.

The next batch of 14 tier-2 outlets collectively drew 8.09M visits in Q2, representing 38.73% of the region’s crypto-native media traffic:

- bytwork.com

- cryptowisser.com

- cryptodnes.bg

- kryptomagazin.sk

- bits.media

- cryptonews.net

- ru.beincrypto.com

- incrypted.com

- profinvestment.com

- cryptorussia.ru

- mpost.io

- kryptomagazin.cz

- kriptoworld.hu

- bitcoinbazis.hu

This concentration of visibility was even more pronounced than in Western Europe, where in Q1 2025 the top 13 outlets (7 top-tier + 6 mid-tier) accounted for 78.26% of crypto-native traffic. And similar to Latin America, which saw 69.13% of traffic consolidated among just six outlets, Eastern Europe’s top two tiers alone drove 80.71% of crypto-native visits – despite an increasingly fragmented ecosystem of smaller sites and niche players.

A group of 29 tier-3 outlets collectively brought in 3.62M visits in Q2, which makes up 17.33% of Eastern Europe’s crypto-native media traffic:

- coinmate.io

- holder.io

- coinspot.io

- pl.beincrypto.com

- bitcoin.pl

- bitstat.top

- fintolk.pro

- cryps.pl

- coindar.org

- crypto.ro

- happycoin.club

- kriptoakademia.com

- block-chain24.com

- getblock.net

- kryptonovinky.cz and 14 more

Finally, at the base of the mediascape lies a vast long tail of 68 niche outlets. While each of these averaged under 10K monthly visits, together they contributed approximately 410.29K visits, making up just 1.96% of the region’s crypto-native media traffic:

- decenter.org

- okchanger.com

- kripto.media

- bitexpert.io

- cryptonica.news

- poradnik-inwestora.pl

- ttrcoin.com

- cryptocurrency.tech

- majning-bitcoin.ru

- 2bminer.com

- and 57 more

Despite their limited reach, these outlets form a decentralized layer of crypto journalism, often catering to highly specific local or thematic audiences.

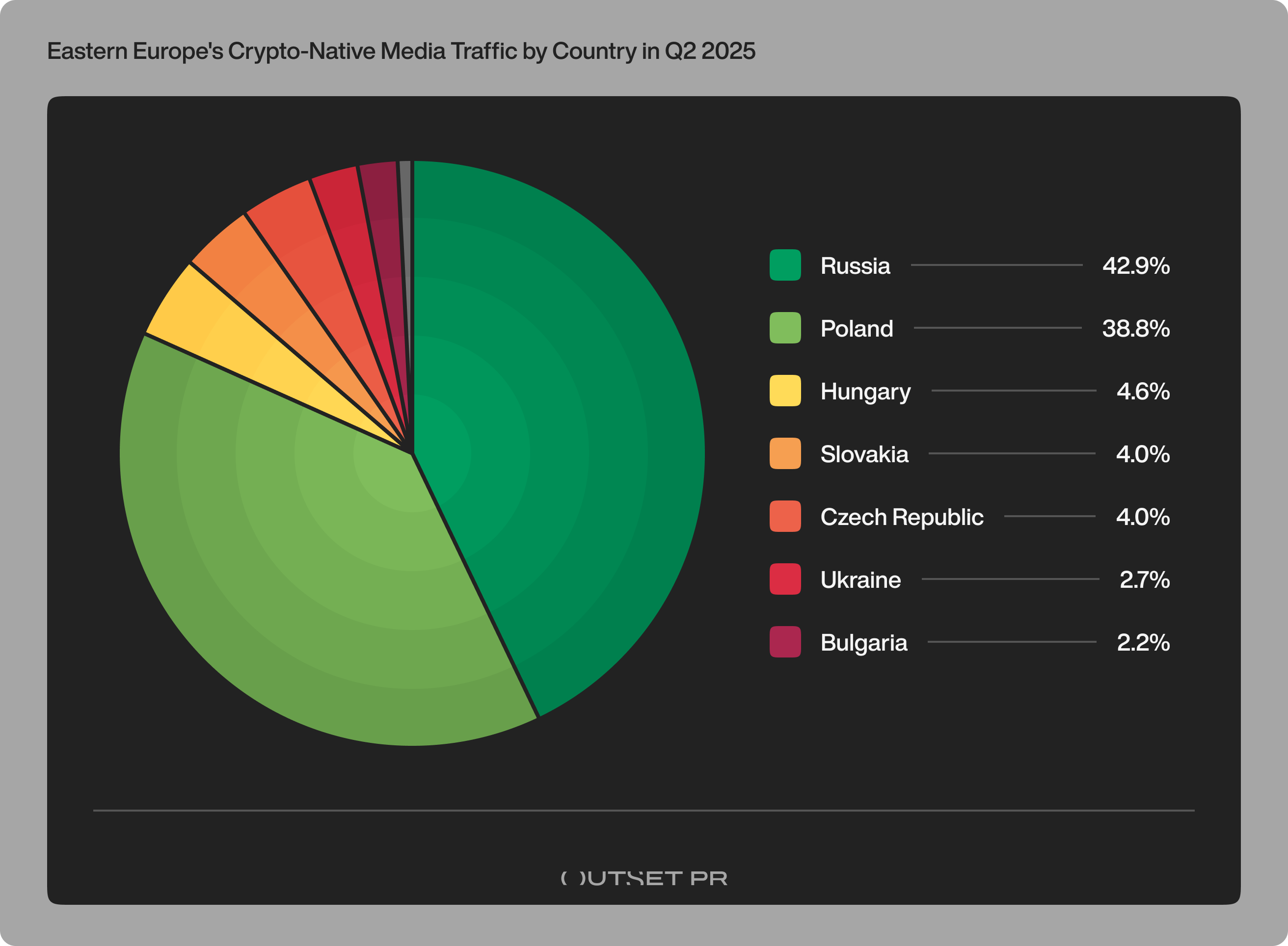

Russia and Poland drive 82% of Eastern Europe’s crypto-native media traffic

To ensure accurate country-level attribution, traffic was adjusted for publishers serving multiple main audiences. Rather than assigning 100% of an outlet’s traffic to a single country, we split it only among its identified Eastern European target audiences.

For example, CryptoDnes.bg had Bulgaria and Japan listed as its main audiences. Since Japan falls outside the regional scope of this report, only the Bulgarian share of traffic was included in the calculation.

In contrast, if an outlet listed Russia, Ukraine, and Belarus as its primary audiences, its traffic was proportionally allocated across those countries, ensuring Eastern European totals reflect real multi-market presence.

Note: Representatives of Incrypted stated separately that, despite SimilarWeb data indicating the presence of a Russian audience, they do not work directly with users from Russia and do not target content to this market.

This methodology provides a regionally grounded view of crypto-native media and offers a more accurate picture of where its visibility truly resides:

- Russia led with 8.44M visits, accounting for 42.89% of the region’s crypto-native traffic.

- Poland followed with 7.63M visits (38.76%), largely driven by dominant outlets like Comparic.pl.

- Hungary contributed 902K (4.58%), with notable influence in regional mid-tier outlets.

- Slovakia and the Czech Republic each recorded around 780–790K visits, with the Czech Republic slightly ahead at 791.96K (4.02%), and Slovakia at 782.53K (3.97%).

- Ukraine followed with 521.97K (2.65%), while Bulgaria reached 426.25K (2.17%).

- Smaller but visible footprints came from Belarus (100.29K / 0.51%), Romania (55.51K / 0.28%), Latvia (22.75K / 0.12%), Croatia (4.85K / 0.02%), and Greece (4.10K / 0.02%).

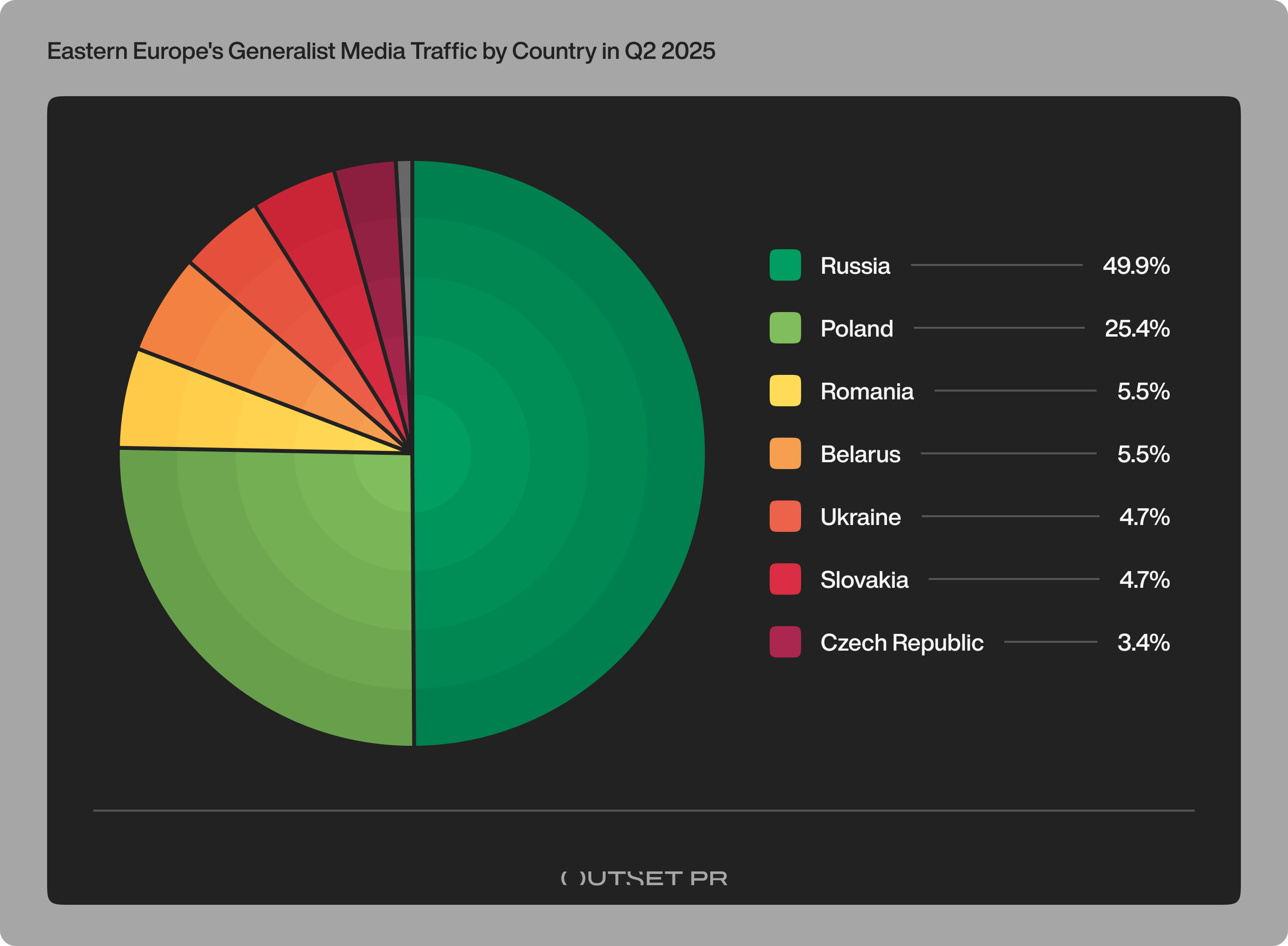

75% of generalist traffic also comes from Russia and Poland

While crypto-native media presents a fragmented yet diverse landscape, generalist media platforms continue to dominate overall reach across Eastern Europe. These broader news and finance outlets, which occasionally cover crypto, collectively attracted nearly 895M visits in Q2 2025 – a volume more than 45 times greater than crypto-native media alone.

Much like the crypto-native segment, traffic from generalist media in Eastern Europe was heavily concentrated in a handful of countries in Q2 2025.

- Russia led by a wide margin with 446.29M visits, accounting for 49.89% of the region’s generalist media traffic.

- Poland followed with 227.03M visits, representing 25.38% of the total.

- Romania and Belarus each contributed just over 5.5% of regional traffic, reflecting notable traction despite a smaller number of outlets.

- Ukraine and Slovakia were nearly tied, accounting for 4.73% and 4.67%, respectively.

- The Czech Republic followed with 3.44%, while Hungary (0.36%) and Bulgaria (0.30%) posted smaller contributions.

- Greece, Estonia, and Moldova each contributed less than 0.25%, indicating very limited reach from generalist platforms in those markets.

Generalist media may have extensive reach, but the figures highlight that Russia and Poland continue to dominate where that traffic actually lands.

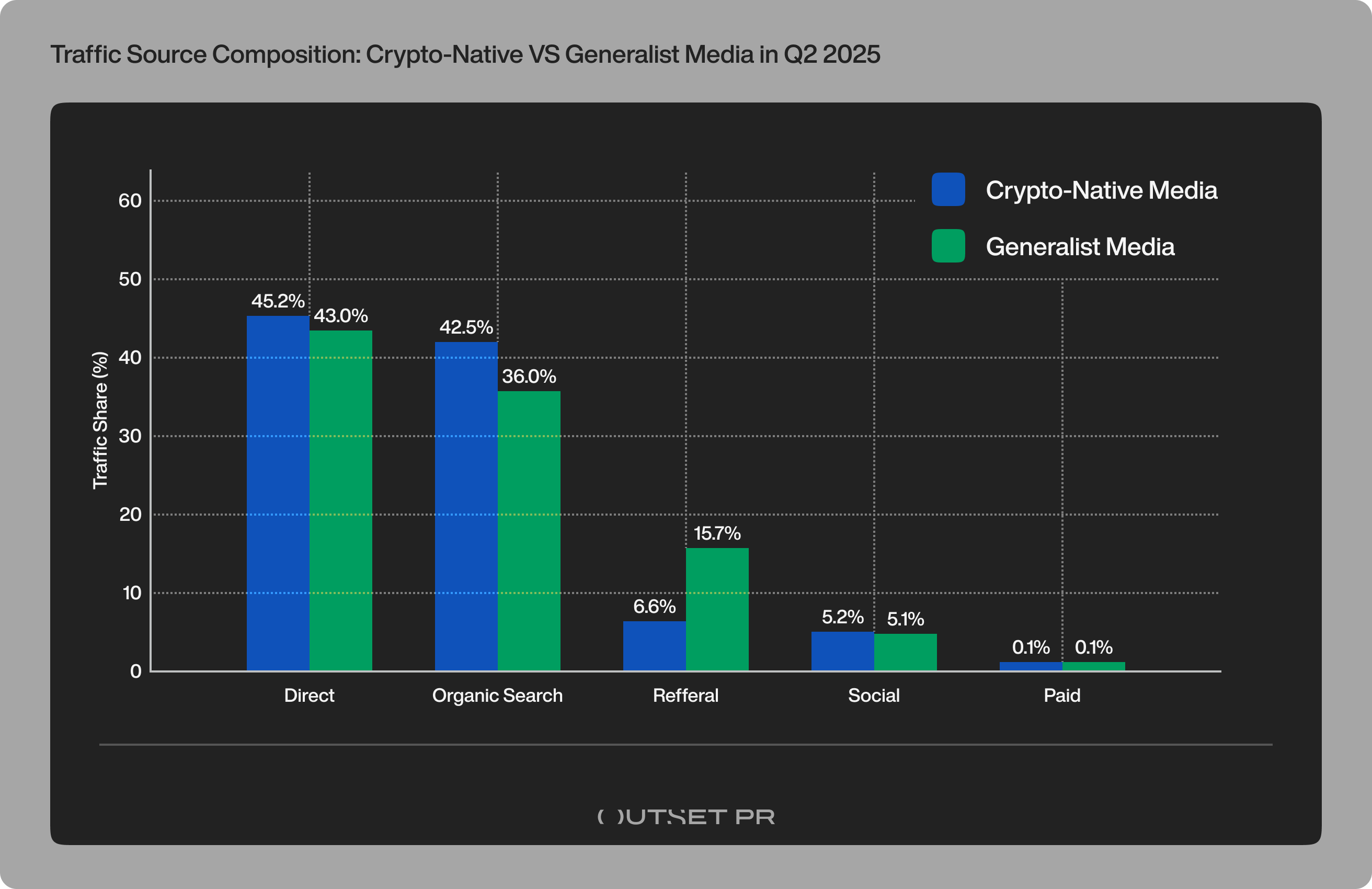

Direct and search dominate, but generalist media drive greater visibility through referrals and scale

To better understand how audiences engaged with crypto-related content in Q2 2025, we analyzed traffic source composition across crypto-native and generalist media outlets.

For crypto-native platforms, traffic was driven primarily by direct visits, which accounted for 45.20% of all sessions – 9.44M visits.

Organic search contributed another 42.47%, or 8.87M visits, confirming that discoverability through search remains important – though it’s often tied to branded or topic-specific queries rather than broad audience capture.

Referral traffic made up 6.57%, or 1.37M visits, with key drivers largely consisting of news aggregators, crypto ranking platforms, community forums, and AI discovery tools.

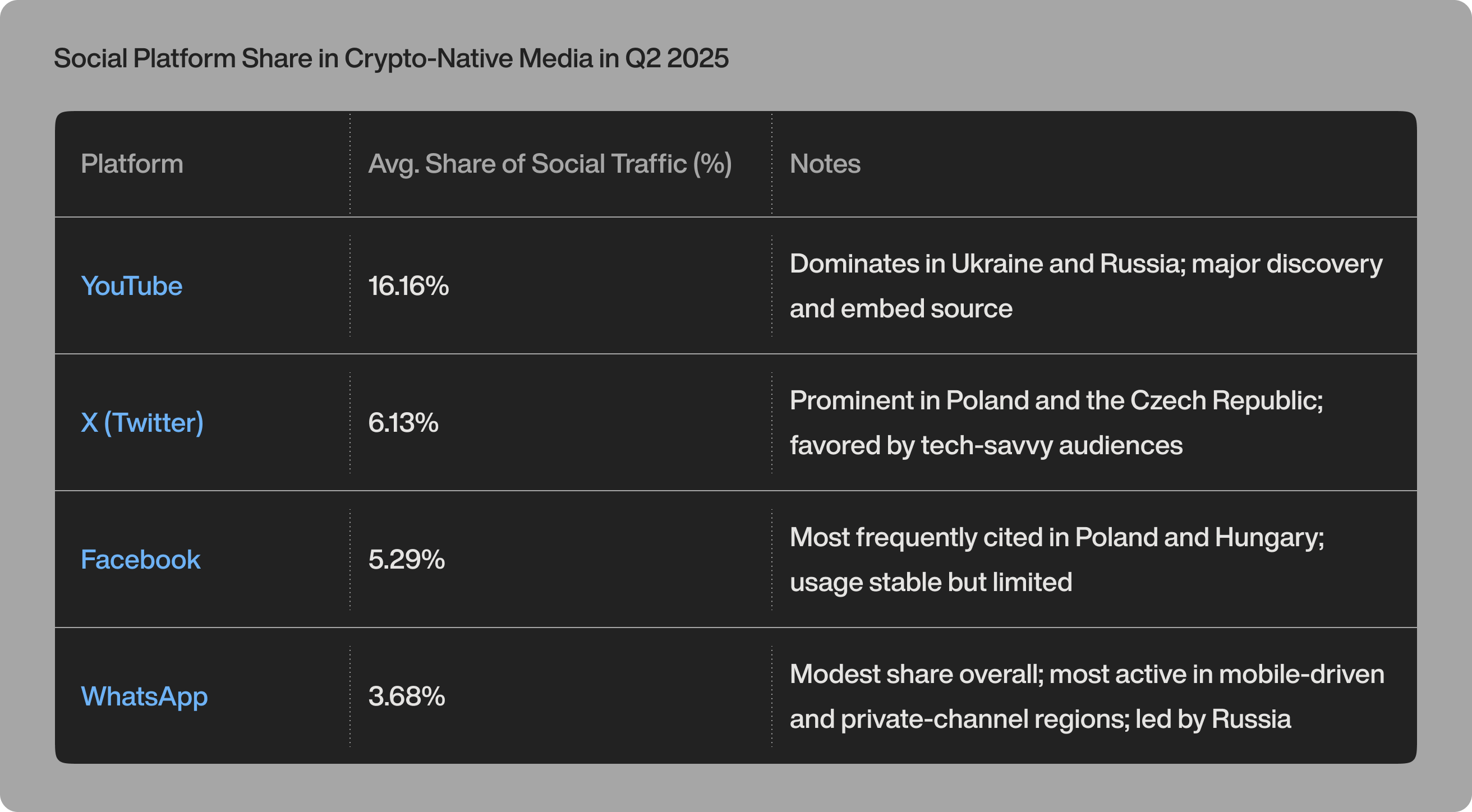

Social media was responsible for 5.23%, or 1.09M visits, with most engagement coming from platforms like Facebook, YouTube, and X, along with smaller inputs from Reddit, VK, and others. While it remains a relatively small contributor to overall crypto-native traffic, platform-level patterns show clear geographic preferences and audience behaviors.

Among all crypto-native outlets reporting traffic composition, YouTube drove the highest share of social traffic in Q2 2025 – 16.16%, or 176,706 visits. It was especially prominent in Ukraine and Russia, where video discovery and embedded content are key engagement formats.

X followed with 6.13% (67,017 visits), reflecting a strong foothold in Poland and the Czech Republic, where it’s favored by tech-savvy and globally connected audiences.

Facebook, contributing 5.29% of social-driven traffic (57,825 visits), was most frequently cited by outlets in Poland and Hungary. While its role has diminished in some regions, it remains a consistent, if secondary, channel for audience interaction.

WhatsApp, though appearing in several breakdowns, accounted for 3.68% (40,211 visits) of tracked social traffic. Its actual influence may be higher, as private or encrypted sharing through platforms like Telegram and WhatsApp often gets recorded as direct rather than referral traffic in analytics tools.

Note: Platforms like Telegram, Instagram, VK, and TikTok were observed but had shares too low to be ranked. Moreover, apps such as Telegram and WhatsApp often mask referrals as "direct" due to encrypted link routing, making their true impact likely underrepresented.

Paid traffic for crypto-native outlets was nearly negligible, contributing only 0.06%, or 12,920 visits, reinforcing their dependence on organic, community-driven visibility.

In contrast, mainstream and generalist outlets that cover crypto as a subtopic exhibited a more diversified traffic composition. While direct traffic remained the top source at 43.04% (385.01M visits), the distribution of other channels revealed key differences:

Organic search contributed 35.97% (321.79M visits), reflecting the effectiveness of institutional SEO strategies and broadly indexed evergreen finance content.

Referral traffic was notably higher at 15.66% (140.10M visits), driven by strong placement in regional aggregators and syndication platforms such as Yandex and Dzen.

Social traffic made up 5.12%, totaling 45.76M visits, largely attributed to Facebook and YouTube, with supporting contributions from X, LinkedIn, and other multi-channel sharing mechanisms (e.g., video embeds).

Paid traffic, though still a minor factor, matched crypto-native outlets at 0.06%, but due to generalists’ scale, this translated to 534,539 visits — showing some use of sponsored content, programmatic ads, or retargeting strategies, particularly among hybrid business and tech publishers.

Beyond these core categories, a small share — 0.5% for crypto-native traffic and 0.2% for generalist traffic — captures unclassified or low-volume sources. In many cases, their real impact is undercounted due to tracking limitations.

Key takeaways:

- Direct and organic traffic dominate both crypto-native and generalist outlets. For crypto-native platforms, these two channels account for 87.70% of all traffic; for generalist media, they contribute a combined 79%, still forming a clear majority.

- Crypto-native media leans more heavily on loyalty-driven direct visits and organic discovery, with virtually no paid traffic.

- Generalist outlets diversify more broadly — achieving higher referral traffic and greater paid visibility in absolute terms, thanks to their much larger reach and syndication footprint.

AI-driven discovery is redefining crypto traffic in Eastern Europe

AI-driven discovery platforms like ChatGPT, Perplexity, Copilot, and others are increasingly reshaping how audiences interact with crypto content. Rather than clicking through from traditional referral sources like Google Search or aggregators, users now often receive summarized responses directly within these AI tools. This shift toward "answer-first" interfaces is changing the anatomy of referral traffic – with fewer visits stemming from speculative search behavior and more readers passively consuming AI-delivered overviews.

As a result, traditional pathways like search and aggregator referrals are yielding fewer conversions. Content that once might have driven substantial clickthroughs is now compressed into AI summaries – reducing referral-based visibility for publishers. This evolving behavior contributes to the overall decline in speculative traffic and signals a broader shift in user expectations.

For crypto media, the challenge is twofold: maintain visibility in classic channels while adapting to a new generation of discovery layers driven by content quality, structured markup, and semantic relevance in AI-generated results.

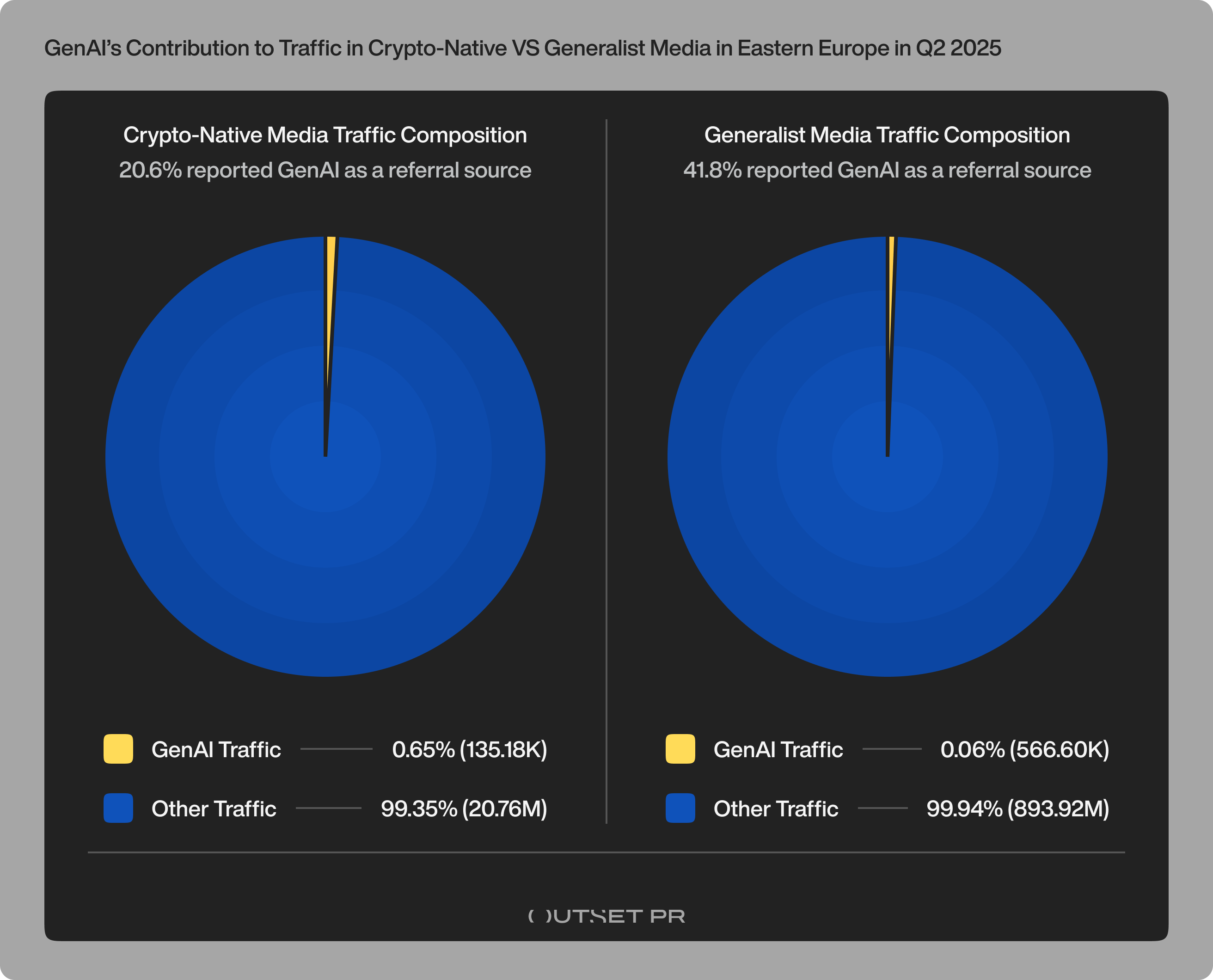

This behavioral shift is clearly reflected in the data. In Q2 2025, GenAI tools such as ChatGPT, Perplexity, Gemini, and Copilot emerged as meaningful traffic drivers for crypto-related media.

AI-driven traffic was recorded by 20.6% of all crypto-native outlets, indicating early but growing adoption across the sector. Based on estimated referral shares, 135,180 visits — or 0.65% of the total 20.89M visits to crypto-native outlets — originated from these AI-powered platforms.

For generalist media, which drew a significantly larger audience with 894.48M total visits in Q2, GenAI platforms played a smaller but still measurable role in traffic acquisition. GenAI tools like ChatGPT and Perplexity were listed as referral sources by 41.8% of generalist outlets — more than double the share seen among crypto-native publishers. Referral data indicates these platforms directed 566,596 visits, representing 0.06% of generalist media traffic.

These figures highlight how AI-driven discovery is becoming a meaningful channel for both niche and mainstream crypto content consumption.

To better understand how publishers perceive the rising influence of AI in crypto content distribution, we conducted an anonymous survey of Eastern European crypto media professionals. Their responses reveal an evolving but cautious recognition of AI’s role in shaping audience behavior.

Many respondents noted a decline in speculative traffic – attributing this drop to how tools like ChatGPT and Perplexity deliver instant answers without requiring a click to the source. As one editor explained:

“I think they have an impact on the decline, since the AI begins to provide an answer to a search query without clicking on links.”

Others observed traffic spikes from emerging GenAI platforms like You.com or Copilot, especially when content is directly linked or summarized:

“Articles getting linked in ChatGPT or You.com can spike for a few hours. But there’s no way to optimize for it... yet.”

Still, most agreed that this traffic remains erratic and unreliable:

“We’ve seen a few bumps from AI tools, but it’s not reliable traffic yet. It’s more like discovery testing.”

Several media teams reported adapting their content structure to be more “AI-friendly” – anticipating a future where language models shape how readers find and engage with crypto news. Others expressed concern over eroding click-through rates due to Google’s AI summaries, while doubling down on their credibility as trusted local sources:

“Traffic from these tools is still marginal vs Google, but we’re monitoring it closely.”

“People trust AI for quick answers – but when they’re investing $10,000, they still want a real source.”

Regulatory complexity and visibility risks

Alongside platform shifts, regulatory frictions continue to shape editorial decisions and media visibility across Eastern Europe. Survey participants from countries including Russia, Ukraine, Hungary, Poland, and Romania described a fragmented and often ambiguous environment shaped by a mix of national laws, EU frameworks, and self-regulatory codes.

In Russia, editors cited the adoption of new laws legalizing crypto mining and preparing for a digital ruble, while simultaneously enforcing strict bans on crypto promotion and gambling-related content. This has directly influenced editorial decisions:

“We don’t accept materials related to gambling due to the ban on its promotion. We comply with the law banning crypto advertising and trading platforms.”

In Ukraine, regulatory progress remained stalled, with no new crypto legislation adopted in 2025. Despite this, local editorial activity remained strong, often guided by internal standards:

“Each site operates individually… we try not to publish scams.”

In Hungary, several respondents pointed to visibility losses following Google Core Updates in early 2025, which they suspect were linked to increased enforcement of MiCA and ESMA guidelines:

“Our traffic dropped substantially, starting in January – likely due to MiCA and ESMA rules. Discover visibility was affected.”

In Poland, outlets referenced adherence to national frameworks, such as the Office of Competition and Consumer Protection (UOKiK) and the Polish Financial Supervision Authority (KNF). These were seen as shaping both content boundaries and audience-facing credibility.

In Romania, teams highlighted EU-wide compliance, particularly with MiCA, and reaffirmed their commitment to high editorial standards:

“We closely monitor and take into account the regulatory frameworks that apply within the European Union… We follow best practices in responsible reporting by fact-checking our content, clearly marking sponsored materials, and avoiding misleading headlines or sensationalism.”

While most participants support responsible publishing, they also noted that compliance doesn’t guarantee discoverability – especially as algorithmic signals shift in response to regulatory sensitivity.

“You follow the rules and still lose ranking, but you can’t risk being flagged either.”

This collision of national law, EU oversight, and algorithmic behavior has made compliance a moving target – one that increasingly determines both what gets published and whether it gets seen.

Get armed with the full dataset

For both in-house communications teams and independent PR agencies, surface-level traffic numbers are no longer enough. At Outset PR, we believe that the most effective campaigns start with real, reliable data. That’s why we go beyond generic estimates – continuously tracking, benchmarking, and interpreting crypto media performance across key regions.

The insights in this report are designed for anyone looking to grow, launch, or refine their presence in Eastern Europe’s crypto market. While we use this intelligence to shape our own strategies, we’re committed to publishing it openly – because smarter media planning shouldn’t be a competitive advantage for a few, but a shared tool for the entire crypto ecosystem.

Got feedback, have input, or need consultancy? Connect with our analytics product manager Sofia: sofia@outsetpr.io

As seen in: ABMedia, Altpoint, Benzinga, BitcoinBázis, Bitcrux, BitScoop, Block Hubs, Blockcruck, BlockNow, Blockorn, Blockphere, Blockpost, BlockReach, Crypto Daily, сryptonews, crypto.news, Cryptowisser, Crypto.ro, Finance Magnates, ForkLog, FXStreet, Happy Coin News, Indovestory, MarsBit, Metaverse Post, Moneytimes, Nabzarz, OvenAdd, PortalCripto, ProfitLine, sgzt.com, SignalPlus, TechBullion, The Coin Republic, The Blockopedia, The Crypto Updates, TradingView